Stars are useful for astrologers to make money from their clients. The financial industry must have learnt business tricks from astrologers. It uses Stars, the Morningstar kind, to fool people and make money!

Morningstar Ratings Busted / Morningstar Fails

There is a symbiotic relationship of mutualism between the industry and Morningstar. Unfortunately for investors, it’s “Catch 22.”

It’s a sad situation for millions of people who save their hard earned money in 401k, IRA, or brokerage accounts, using mutual funds and ETFs. They don’t realize that their nest-eggs are being damaged or even destroyed.

Investors are to blame for this dangerous situation. They lack investment know-how and use Morningstar’s Star Ratings to make investment decisions.

Investors should beware of the defects and tricks inside Morningstar’s Star Rating System.

First and foremost, the mathematical foundation of the Star methodology is seriously flawed. It gets an F (FAIL) grade, even as a freshman year Finance-101 paper.

If someone thinks that math is not important in finance, then think again. There is another serious problem. The financial industry and Morningstar’s Stars have conflicts of interest with investors — like a fox guarding the hen-house.

Beyond the conflicts of interest, there is yet another problem. Morningstar’s Stars don’t work. In fact, they are an easy way of losing money.

A Mind-boggling Problem

There are about 326 million people in 126 million households(1) in the U.S. About 95 million people from 25 million households have invested $20 trillion in mutual funds and ETFs(2), but are losing billions of dollars each year, due to mediocre or below market performance.

Investors generally use Morningstar’s Star ratings to make investment decisions. But the Stars don’t work. They are endangering the nest-eggs of millions of families.

Morningstar’s Star Rating Method Is Seriously Flawed

The Star rating method(3) is based purely on Morningstar’s arbitrary definition of fund performance, and is riddled with untested assumptions. There is no mathematical basis to claim predictive value.

The Stars have many hidden pitfalls:

- Unlike Morningstar’s assumptions, investors don’t make decisions using a utility function. Risk tolerance changes with investors’ personal preferences, and a fixed tolerance factor of 2 used in the ratings, is untested.

- A 5-Star fund in one peer group could actually have lower risk-adjusted return than a 2-Star fund from a different peer group. This makes it impossible to compare funds across different peer groups or sectors.

- Arbitrary weighting of Stars going back to 10 years defies logic and is untested. Returns and volatility can change over short intervals in today’s global markets.

Conflicts of Interest — Fox Guarding the Henhouse

The goals of the industry are inherently in conflict with those of investors(4). The industry gets guaranteed fees for its products and services. Since returns cannot be guaranteed, investors can only buy “hope.”

Stars are used to advertise funds, support sales and prove fiduciary responsibility.

Investors are oblivious of what’s going on behind the scenes. Morningstar makes money selling ratings to the industry, and the industry makes money using the ratings to make money! This symbiotic relationship of mutualism can continue forever.

Unfortunately for investors, it’s “Catch 22.”

The Stars Don’t Work

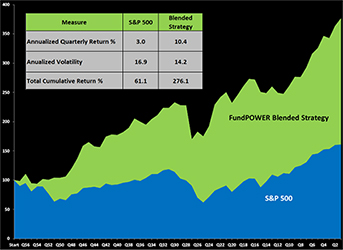

In my experience, the Star Ratings don’t work. Industry publications are raising similar alarms. I don’t use the Star ratings for my own mutual fund and ETF investments.

For a client, I tested the relationship between total returns produced by funds over the next year, and their Star Ratings of the previous year. I did not see any meaningful relationship.

I tested funds with 2-Star to 5-Star ratings for 2009 through 2011, versus their average returns in years 2010 through 2012, and versus their sector averages. For two out of three years, 3-Star funds gave higher returns than 5-Star funds. The average returns were about the same as their sector averages.

A white paper published by Loring Ward(5) also showed that the Morningstar Overall Rating is not a good indicator of future performance.

Morningstar has admitted on several occasions that its Star ratings are only awards for past performance. Yet the firm insists that its Star ratings are useful for making investment decisions!

Articles in publications including Forbes(6), The Wall Street Journal(7), The New York Times(8), Fiduciary News(9), and more recent articles in the Wall Street Journal(10), and Investment News(11), have all raised alarms about the dangers of using Morningstar’s Star ratings.

Their overall message: The Stars have no predictive value. They only represent past performance.

Sources

1: “The State of Wealth Management in 2017,” by Joshua M. Brown, April 17, 2017: http://thereformedbroker.com/2017/04/05/the-state-of-wealth-management-in-2017/

2: “2017 Investment Company Institute, Fact Book,” 57th Edition: www.icifactbook.org

3: “Morningstar Star Rating for Funds,” by Morningstar Inc., November 2016: https://corporate.morningstar.com/US/documents/MethodologyDocuments/MethodologyPapers/MorningstarFundRating_Methodology.pdf

4: “Guidance Information, Ratings, Past Returns and Investors’ Herd Behavior,” by FundPOWER, November 15, 2017. https://efundpower.com/blog/guidance-information-ratings/

5: “Overcoming the Morningstar Heuristic — Addressing Investor’s Star Rating Anchoring Bias,” by Loring Ward Securities Inc: https://loringward.com/

6: “Ignore Morningstar’s Stars,” by Michael Maiello, Forbes, January 30, 2009: https://www.forbes.com/2009/01/29/mutual-funds-morningstar-intelligent-investing_0130_morningstar.html#6c0307023cb9

7: “Investors Caught with Stars in Their Eyes,” by Sam Mamudi, WSJ, 6/1/2010: https://www.wsj.com/articles/SB10001424052748703957604575272461840998720

8: “The Mutual Fund Merry-Go-Round,” by David Swensen, August 13, 2011, Sunday Review Opinion, New York Times: http://www.nytimes.com/2011/08/14/opinion/sunday/the-mutual-fund-merry-go-round.html?nl=todaysheadlines&emc=tha212

9: “Morningstar Star Ratings: Do They or Don’t They Predict?” by Christopher Carosa, January 29, 2013, Fiduciary News: http://fiduciarynews.com/2013/01/morningstar-star-ratings-do-they-or-dont-they-predict/

10: “The Morningstar Mirage,” by Kirsten Grind, Tom McGinty and Sarah Krouse, Wall Street Journal, October 25, 2017: https://www.wsj.com/articles/the-morningstar-mirage-1508946687

11: “Advisers: Morningstar’s star ratings not much use, but clients love them,” by John Waggoner, August 26, 2017, Investment News: http://www.investmentnews.com/article/20171026/FREE/171029954/advisers-morningstars-star-ratings-not-much-use-but-clients-love-them?issuedate=20171031&sid=INTEL&utm_source=MarketIntel-20171031&utm_medium=email&utm_campaign=investmentnews&utm_visit=562611&itx%5bemail%5d=&itx[email]=

About the Author

Since 2007, Dr. Ani Chitaley has been consulting in equity market quantitative research, investment management, performance measurement and trading systems. He is currently working with Investor Empowerment Inc., a FinTech business that provides independent ratings and analysis of mutual funds and ETFs to people who prefer to manage their own investments.

He worked in Fidelity’s mutual fund management division for 11 years, and left Fidelity in 2007 as Senior VP & head of equity market quantitative research.

Ani’s work saved trading costs over $1 billion for Fidelity’s mutual funds. The trade quality measurement system developed under his guidance was used during a major industry-wide SEC investigation, to verify that Fidelity’s trading floor maintained “best-execution” fiduciary responsibility. His team also developed innovative solutions for electronic crossing networks, and algorithmic trading.

In the past, Ani has worked in research and manufacturing management and as a management consultant at Booz-Allen-Hamilton.

He has a doctorate in Mechanical Engineering from MIT, an MBA from Case Western University, and a Masters from IIT, Mumbai, India. He holds patents on volatility based pricing, and on Monte-Carlo based volume-sensitive trade price estimation. Ani can be reached at ani.chitaley@live.com and on LinkedIn.